Why You Need a Business Valuation

An up-to-date business valuation is an increasingly important strategic tool you can leverage to prepare for evolving business and personal situations. With a current valuation in hand, you will be prepared for unforeseen circumstances and opportunities—and armed with valuable insights that will enable you to make more informed decisions.

From a business perspective, a valuation is a key factor in obtaining bank financing, venture capital, or capital from other investors if your growth plans require additional funding. Your growth plan, or exit strategy, may also necessitate a comprehensive valuation to more successfully negotiate and evaluate transactions such as a partnership investment or buyout, merger or acquisition, strategic sale, or Employee Stock Ownership Plan (ESOP). And if you are beginning to contemplate an exit strategy, a valuation establishes a baseline value for your company. It is the first step in developing a plan to improve profitability and increase the company’s value.

On the personal side, a valuation also plays an important role in estate planning. It is an essential element regarding transfers for gift tax, whether you’re granting ownership interest to a family member or donating to charity.

On the personal side, a valuation also plays an important role in estate planning. It is an essential element regarding transfers for gift tax, whether you’re granting ownership interest to a family member or donating to charity.

And then there are those unexpected and unpleasant situations where a current business valuation is critical: like in business disaster planning to obtain proper insurance coverage, and in the event of shareholder or partner disputes.

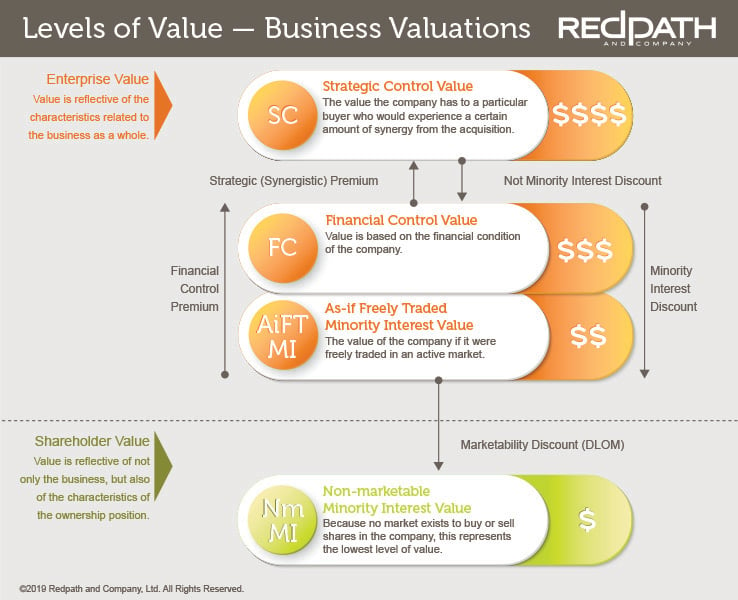

Standard of Value

The standard of value relates to, and is driven by, the purpose of the valuation and helps answer the question, "What do you mean by value?"

The standard of value and the context in which it is used will influence the approaches and methodology used in the valuation. The applicable standard of value should be identified and defined as part of any valuation engagement. There are four main standards of value, each with numerous inherent assumptions that represent the basis of the valuation:

The standard of value and the context in which it is used will influence the approaches and methodology used in the valuation. The applicable standard of value should be identified and defined as part of any valuation engagement. There are four main standards of value, each with numerous inherent assumptions that represent the basis of the valuation:

- Fair Market Value

- Fair Value

- Investment Value

- Intrinsic Value

These assumptions will shape the application of the valuation approaches and methodologies.

Fair Market Value

Fair market value is one of the most widely recognized and accepted standards of value. Given its use for virtually all federal and state tax matters, the most prominent definition for fair market value comes from the U.S. Treasury regulations.

They define fair market value as the price at which the property would change hands between a hypothetical willing buyer and a hypothetical willing seller, acting at arm’s length, when neither is under compulsion to buy or sell and when both have reasonable knowledge of the relevant facts.

While fair market value is the standard of value utilized by the IRS, it is also commonly applied in judicial matters, used in buy-sell agreements and for other valuation situations.

Fair Value

Fair value is a more complex standard of value with numerous definitions that depend on the context in which it is applied. Fair value can be the prevailing standard of value used in a number of situations, including financial reporting, dissenting shareholder, and certain transactions.

For matters involving financial reporting, fair value is defined by the Financial Accounting Standards Board (FASB) as “the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date.”

The FASB definition is similar to the definition of fair market value in how it’s applied, but does not consider any discounts. This nuanced approach to fair value is important to understand. The definition of fair value can become a legal question as many states now have statutory fair value definitions.

Investment Value

Investment value considers the value of a company from the perspective of a buyer or current owner.

While investment value is not a typical standard of value utilized by valuation analysts, it does make its presence in family law occasionally. While not always described as investment value, courts can look to the value of business in the hands of a particular owner.

Intrinsic Value

This standard of value is not often used in any meaningful way for business valuation purposes, but the concept itself is worth noting.

While this sounds slightly like investment value it is important to note that investment value is derived from the beliefs and thoughts of a particular owner or individual, while intrinsic value represents the perceived value based on the characteristics of a particular company.

Go in-depth with our Insights on Business Valuation to help you make decisions that are best for you.

Whether you're deciding if a Business Valuation makes sense for you or you're trying to calculate your company's value, we have the article for you.

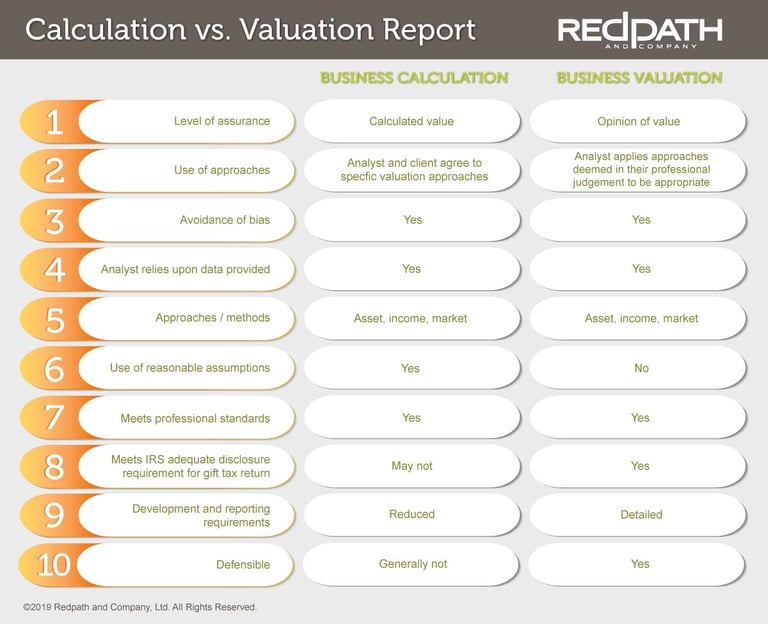

Business Calculation Report vs. Business Valuation Report

There are two levels of service a business valuation analyst can offer: Business Calculation Report and Business Valuation Report.

The two may sound similar, but they are actually very distinct. A expert valuation analyst can help business owners review the facts and circumstances of the situation and determine which type of engagement makes the most sense.

Business Calculation Report

Business value calculation is a less detailed analysis of business valuation. You can use a business value calculation for planning and strategy development, preliminary negotiations, or when a full business valuation is not practical due to time and budget constraints. The exact methods are discussed and agreed to before any analysis begins. It costs less to have this form of valuation completed, and it takes less time, but its applications are limited.

Business Valuation Report

Business valuation involves a conclusion of value. To get there, your analyst needs to do more research and analysis than in a business value calculation. In a business valuation, he or she will look at the value of your company using appropriate approaches (asset, income, and market) and methods. To arrive at a conclusion of value, your analyst will also look at your company’s history, financial statements, and a number of other factors. A conclusion of value in a business valuation report is the analyst's opinion regarding the value of the business. The analyst should be able to support and defend their position against the IRS, a court of law, or other authority.